Huntsworth is an open restricted organization headquartered in London and recorded on the London Stock Exchange. In this article, you will get the Ratio Analysis of Huntsworth Plc. Huntsworth is a social insurance correspondence and advertising bunch working from 62 vital workplaces in 29 nations giving administrations to 1, 870 customers. The gathering works in the shopper, monetary, open issues, coordinated medicinal services, and innovation parts and includes four divisions being Huntsworth Health, Grayling, Citigate, and Red. Huntsworth plc works as a human services correspondences and advertising organization in the United States, United Kingdom, rest of Europe, Asia, and the Middle East and Africa. It works through four divisions: Huntsworth Health, Red Consultancy, Grayling, and Citigate Dewe Rogerson (CDR).

The Huntsworth Health division offers an incorporated suite of interchanges administrations for the science, wellbeing, and prosperity enterprises. The Red Consultancy division gives creates and oversees battles, runs squeeze workplaces, and steers brands and organizations through a commitment to media, buyers, client partners, and inside gatherings of people. Huntsworth PLC is a global medicinal services correspondences and advertising gathering. It is adjusted under four central divisions including Huntsworth Health, Citigate, Grayling, and Red.

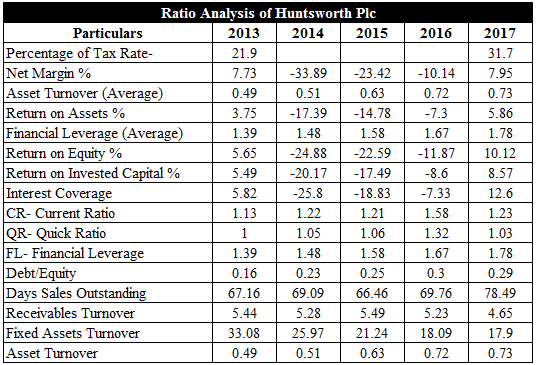

Ratio Analysis of Huntsworth Plc

| Ratios | 2013 | 2014 | 2015 | 2016 | 2017 |

| Operating Margin % | 13.1 | 11.4 | 8.6 | 9.9 | 11.9 |

| EPS -Earnings Per Share 9EPS) GBP | 0.05 | -0.17 | -0.12 | -0.06 | 0.05 |

| Dividend GBP | 0.04 | 0.04 | 0.01 | 0.02 | 0.01 |

| The Payout Ratio % * | 63.6 | 92.1 | |||

| Shares Mil | 271 | 319 | 321 | 329 | 335 |

| Book Value Per Share * GBP | 0.7 | 0.77 | 0.45 | 0.46 | 0.46 |

| Operating Cash Flow GBP Mil | 13 | 14 | 12 | 9 | 23 |

| Cap Spending GBP Mil | -3 | -5 | -3 | -6 | -2 |

| Free Cash Flow GBP Mil | 10 | 9 | 9 | 2 | 21 |

| Free Cash Flow Per Share * GBP | 0.04 | 0.04 | 0.04 | 0.03 | |

| Working Capital GBP Mil | 7 | 10 | 10 | 30 | 16 |

| Profitability | |||||

| Sales Margin | 2013 | 2014 | 2015 | 2016 | 2017 |

| Sales Revenue | 100 | 100 | 100 | 100 | 100 |

| COGS | |||||

| GPM- Gross Profit Margin | |||||

| SG&A | 18.39 | 21.91 | 23.1 | 21.18 | 20 |

| R&D | |||||

| Other | 68.52 | 66.72 | 68.34 | 68.92 | 68.14 |

| Operating Margin | 13.09 | 11.38 | 8.56 | 9.9 | 11.86 |

| Net Int Inc & Other | -3.19 | -47.31 | -32.21 | -19.06 | -0.22 |

| EBT Margin | 9.89 | -35.93 | -23.65 | -9.16 | 11.64 |

| 2013 | 2014 | 2015 | 2016 | 2017 | |

| Percentage of Tax Rate- | 21.9 | 31.7 | |||

| 1. Net Margin % | 7.73 | -33.89 | -23.42 | -10.14 | 7.95 |

| 2. Asset Turnover (Average) | 0.49 | 0.51 | 0.63 | 0.72 | 0.73 |

| 3. Return on Assets % | 3.75 | -17.39 | -14.78 | -7.3 | 5.86 |

| 4. Financial Leverage (Average) | 1.39 | 1.48 | 1.58 | 1.67 | 1.78 |

| 5. Return on Equity % | 5.65 | -24.88 | -22.59 | -11.87 | 10.12 |

| 6. Return on Invested Capital % | 5.49 | -20.17 | -17.49 | -8.6 | 8.57 |

| 7. Interest Coverage | 5.82 | -25.8 | -18.83 | -7.33 | 12.6 |

| 8. Growth | |||||

| 2013 | 2014 | 2015 | 2016 | 2017 | |

| 9. Liquidity | |||||

| 10. CR- Current Ratio | 1.13 | 1.22 | 1.21 | 1.58 | 1.23 |

| 11. QR- Quick Ratio | 1 | 1.05 | 1.06 | 1.32 | 1.03 |

| 12. FL- Financial Leverage | 1.39 | 1.48 | 1.58 | 1.67 | 1.78 |

| 13. Debt/Equity | 0.16 | 0.23 | 0.25 | 0.3 | 0.29 |

| 14. Efficiency Ratios | |||||

| 2013 | 2014 | 2015- | 2016 | 2017 | |

| 16. Days Sales Outstanding | 67.16 | 69.09 | 66.46 | 69.76 | 78.49 |

| 17. Days Inventory | |||||

| 18. Payables Period | |||||

| 19. Cash Conversion Cycle | |||||

| 20. Receivables Turnover | 5.44 | 5.28 | 5.49 | 5.23 | 4.65 |

| 21. Inventory Turnover | |||||

| 22. Fixed Assets Turnover | 33.08 | 25.97 | 21.24 | 18.09 | 17.9 |

| 23. Asset Turnover | 0.49 | 0.51 | 0.63 | 0.72 | 0.73 |

Ratio Analysis

Activity Ratios

The extents of the action are utilized to measure how an association utilizes its advantages. The extents offer monetary masters thought of the general operational execution of an organization. As ought to be evident in Table 1, shared activities are extents of “development” that influence a compensation clarification line thing in financial detailing detail. As illuminated in my past articles, the announcement of installments estimates execution for a predefined period, while the cover the set-up presents data that starts at a particular time. To make things proportionate to their utilization in extents of development, a typical figure is resolved for money related enroll data utilizing the begin and finish numbers declared for the period (quarter or year). The extents of activity measure the speed at which the association is changing its advantages or obligations. In a manner of speaking, they present how regularly every year the inventories are energized or the credits are gathered.

Stock turnover

Stock turnover is figured by isolating the cost of products sold for typical stocks. A turnover higher than ordinary business infers that the stock is sold at a speedier pace, denoting the ampleness of the organization. Then again, a high turnover rate of the association infers that fewer exercises are tied up in the distribution center. Nevertheless, there are generally opposite sides in the record of any extent. A shockingly high stock turnover rate might be a sign that an association’s stocks are unnecessarily low and the organization will most likely be unable to stay aware of any broadened request. Besides, the distribution center trade is to a great degree particular for the division. In an industry where the save rapidly ends up malodorous, you should search for associations with a high offer turnover. For our situation in Table 1, the extent of turnover of 2.6 times suggests that the offers have been “conveyed” or restored 2.6 times inside a year. (This is contrasted with the capacity to be conveyed once every 140 days, or 365 days ÷ 2.6). The sum utilized, $ 190 million, decides the utilization of a $ 180 million start-up share as of December 31, 2010, and a culmination of the $ 200 million stock as of December 31, 2011. $ 190 million addresses the typical stock, held in mid-2011, the day and age at which $ 500 million is delivered in the cost of products sold. Going ahead, a diminishing in inventories or a development of the cost of items sold will expand the extent, denoting more prominent effectiveness of (offering a comparable proportion of products while holding less or offering more merchandise while keeping up a comparative proportion of activity).

Receivables Turnover

The level of credit turnover is dictated by detaching net salary from normal advances. This extent is a proportion of the speed and fitness of an association on its remarkable solicitations. Credit turnover indicates how regularly the association registers and credits for the period. In Table 1, the turnover of the advances is 7.8 times, underlining that, in general, the credits were completely gathered 7.8 times in the period or once every 47 days (365 ÷ 7.8). Little by little, high turnover with the contribution of the affiliation’s opponents. A high level of credit turnover may likewise infer that an association’s credit approach is unnecessarily serious, causing action, making it difficult to pass a vast opening chance. Then again, low or falling deals may show that clients are endeavoring to pay their bills.

Payables Turnover

The payable turnover estimates how rapidly an association pays cash owed to providers. Relative buys (for possible later use) of ordinary obligations. Our invoicing of 5.8x in charges shows that, 5.8 times in the period or once every 63 days (365 days – 5.8). Obligation deals increment as more buys are made or when an association builds its payable records. A high number as opposed to the business and the other way around. A bizarrely high extent may have been proposed for this reason. A low rate of installment pivot could demonstrate that an association has issues paying their bills or exploiting credit comes nearer from liberal suppliers. Make certain to subdivide the models in the charging proportion, as a redress later on. What’s more, industry principles can contrast definitely.

Asset Turnover

It measures to what extent an organization uses its aggregate benefits to generate revenue. Income disaggregated by normal aggregate resources. Our profit gains of 0.72x indicated that the company earns $ 0.72 of revenue for the $ 1 of benefits the organization incurred. It is a waste in the use of its benefits or that it is a function of a condition of capital escalation. In addition, it could be a key point for a capital escalation approach.

Liquidity Ratios

The proportions of liquidity are the proportions most widely used, perhaps beyond the proportions of productivity. They are particularly critical for tenants. These proportions measure the capacity of an association to meet its fleeting commitments. The level of liquidity required by the industry for the industry. Increase of others. For example, it will require more stock purchases than the programming companies, to discover the liquidity of the organizations in these two companies in proportions of liquidity after a time.

Current Ratio

The current percentage of an organization’s current resources. A presentation of the presentations of the organization of the payment system. Claims and actions, and others, the highest point of the good. A low level of participation in the short term and the facilitated examination deserves. For example, a gift of less than 1.00x. Here, the company is working with a current low ratio of 0.91x. It has been shown to be 91% of CL- current liabilities. So, therefore, the high percentage shows an irregular or abnormal result state of liquidity. A current ratio that is too high. Although these problems will not cause a rapid bankruptcy, they will surely damage the main concern of the organization.

Quick Ratio

The quick ratio proportion is a proportion of liquidity that is stricter than the present proportion. This relationship thinks about cash, without further ado alluring qualities and records receivable of current liabilities. The thought behind the speedy relationship is that security subtle elements, for instance, prepaid expenses, have quite recently been paid for quite a while later and can not be rapidly and effortlessly changed to cash for liquidity purposes. For our situation, the speedy proportion of 0.45x demonstrates that the association can just take care of 45% of the expense, utilizing the cash in the region, offering alluring qualities without further ado and adjusting the obligation claims. The genuine detail rejected in the dynamic relationship is the stock, which can constitute a lot of current assets, however, it can not effortlessly be traded for cash. In the midst of weight, high inventories of all associations in the business can make tricky activities be advertised. Also, if the stores of the association are too specific or obsolete, they can be worthless for a conceivable purchaser. Consider Apple Inc. (AAPL), for instance, which is known to utilize particular pieces for your articles. If the association hopes to offer offers rapidly, the stores it is transmitting might be supported, paying little respect to the span of the offers it carries on its books.

Cash Ratio

The most preservationist liquidity proportion is the extent of cash, which is spoken to as a wellspring of cash and at this very moment, appealing qualities isolated by current liabilities. Cash and without further ado alluring qualities talk about the most liquid assets of an organization. Without a moment’s hesitation, appealing qualities join at this very moment too many liquid assets, for instance, consulted in an open market, activities, qualities, and decisions that stay underneath what one year. Amidst run of the mill monetary circumstances, these securities can be sold absent much exertion in an activity. The business connection of Table 1 is 0.27x, which suggests that the organization can just cover 27% of its present liabilities with its cash and here and alluring qualities. In spite of the fact that this proportion is by and large considered the most direct and outstandingly solid, it is possible that even without a moment’s hesitation appealing qualities can be found in a colossal drop in costs.

Solvency Ratios

The extents of the disintegration limit measure the limit of an association to satisfy its long haul responsibilities. The disintegration extents examine gives information about the capital structure of an association and, likewise, the level of utilization of the financial backing utilized by an organization. Some weakening proportions enable budgetary authorities to check whether an organization has attractive money streams to dependably pay premium portions and other exchanged charges. If an association does not have adequate money streams, the organization is without a doubt overburdened with the bondholders and can drive the association to default.

Debt to-Asset Ratio

The commitment asset relationship is the most basic explanation behind the disintegration while evaluating the level of total assets of an association that is financed by commitment. The proportion is computed by isolating all liabilities by including assets. A high number implies that the organization is utilizing a bigger proportion of fiscal utilize, which stretches out its hazard identified with cash as premium portion installments. For our situation in Table 1, the total of liabilities speaks to 72% of aggregate assets.

Debt to-capital Ratio

The relationship between the obligation and capital is fundamentally the same when estimating the measure of aggregate capital (liabilities in addition to the value) of an organization that is given by the obligation (intriguing notes and short and long term). Little by little, a high proportion implies a high use and risk related to money. Although the use related to money is an additional monetary risk due to the extension of payments on preferential terms, the main advantage of using the loan is that it does not weaken the property. In principle, revenues are part of fewer owners, obtaining higher earnings per share. Be that as it may, the greater danger related to money related to greater use can cause the organization to maintain more stringent agreements. These agreements could limit the development openings of the organization and the ability to pay or increase benefits.

Debt-to-equity Ratio

The obligation-value relationship measures the measure of the obligatory capital against the uses of the company in contrast with the measure of the value capital that it employs. A ratio of 1.00x shows that the company uses a measure of obligation. Indistinguishable form the value and declares that he is entitled to all the benefits, leaving nothing for the investors in the case of a hypothetical liquidation. For our case, adding to the obligation used as part of the numerator incorporates a short and long term obligation. This relationship can also be determined using the long-distance obligation in the numerator.

Interest Coverage Ratio

The ratio of the scope of the premium also called the premium of the circumstances gained, measures the money flows of an organization created in contrast to its advantageous actions. The ratio is calculated by separating the EBIT (benefit before intrigue and evaluations) by terms of intrigue. In the illustration used as part of Table 1, the 2.3x upper range index shows that the company’s revenues before the intrigue and the rates are 2.3 times more advantageous for the period. The higher the figure, the less likely an organization has to neglect the fulfillment of its payment commitments. A high figure implies that an organization produces a solid income in contrast to its advantage commitments. With proportions of the scope of the intrigue, it is vital to divide them in the middle of large and thin years. Most organizations will indicate a great variety of intrigues in the midst of solid monetary cycles, however, the scope of the intrigue can quickly weaken amidst financial slowdowns.

Profitability Ratios

The proportions of gain are apparently the most used in the speculation test. These proportions incorporate the generalized “edge” proportions, for example, gross income, labor, and net general income. These proportions measure the capacity of the association to obtain satisfactory performance. When breaking the boundaries of an organization, it is constantly judicious to look at them against those in the business and their close rivals. The edges will change between companies. Organizations that work in companies where articles are generally “merchandise” (articles repeated effectively by different companies) will generally have low edges. Companies that offer unique items with high obstacles to the passage, for the most part, have high edges. In addition, organizations can have key upper hands that cause expanded borders.

Gross profit Margin

The gross profit margin as GPM is just the gross pay (salary less the cost of the stock sold) isolated by the net wage. The extent mirrors the valuation choices and the expenses of the things. Half of the gross edge for the association for our situation demonstrates that half of the salary made by the organization is utilized to pay the cost of the stock sold. For most organizations, the net salary will last as the contention increments. If an association has a higher gross pay than the task of the plant in its industry, it is probably going to have a favorable position regarding quality, acumen or stamping, which enables the organization to charge more for its articles. Then again, the organization can likewise have a favorable position in the expenses of the articles because of the viable methodology of creation or economies of scale. Keep in mind that if an association is the first to move and has enough sharp melodies, the candidates will look for ways to deal with the shopping center, which for the most part gives forces to the sliding edges.

Operating Profit Margin

Add up to Operating Profit Margin as OPM is figured by detaching the work wage (net installment short work costs) by net salary. The working edge in Table 1 is 18%, which recommends that for each $ 1 of pay made, $ 0.18 stays subsequent to deducting the cost of stock sold and working expenses. Work costs incorporate expenses, for instance, administrative overheads and diverse costs that can not be credited to singular units. Working Edge watches the association amongst exchanges and costs controlled by the administration. A large portion of the working edge is viewed as a better than average sign, in any case, money related pros must search for strong and solid working edges.

Net Profit Margin

The net income analyzes the net payment of an organization to its net income. This proportion is determined by separating the net salary, or the main concern of an organization, by the net income. The ability of an association to interpret the benefits for the benefit of investors is measured. Gradually, financial investor as an analyst as specialists should consider looking for an organization with the solid as well as the reliable net income.

ROA and ROE

The two other efficiency files are additionally utilized: (ROA) and (ROE).

The advantage of the assets is figured as the net compensation isolated by the whole of the assets. It is a proportion of how successfully the organization utilizes its advantages. A high extent infers that the association can create productively utilizing its advantages. As an assortment, a few specialists accept the open door to decide the arrival of assets from pretax profit and before the top-notch utilizes EBIT isolated by the total assets.

While the arrival of assets estimates the net compensation, which is come back to the holders of the esteem, against the total of assets, which can be financed by commitment and esteem, the proportions of profit for the estimation of the net an incentive for the financial specialist. It gauges the level of credit allowed to financial specialists against the theory that speculators add to the organization. Consider the degree of commitment or utilize identified with cash for work in the organization. Utilize identified with cash enhances the impact of pay on the ROE in great and awful years. On account of expansive blunders between the entry of assets and the advantage by esteem, the organization could join many. As a rule, it is sensible to nearly review the extents of liquidity and solvency.

The mark for our situation in Table 1 has a ROA of 5.6%, which demonstrates that for each $ 1 of assets in the association, the firm is making $ 0.056 in net compensation. The ROE for our situation of 20% suggests that for each estimation of $ 1 in the speculator, the organization accepts $ 0.20 in the net figure.

Written by

Email: [email protected]