CHAPTER ONE: INTRODUCTION

1.1 Background of the Study (Development of Mobile Payment in China)

In the present day and age today, the improvement of portable installment applications and systems have experienced critical change and have made a stride towards positive development. As instilled by a report dispatched by Erikson (a worldwide correspondence arrangements and administrations supplier organization) in November 2012, there were approx. 7.5 billion clients of a cell phone, much more than the number of inhabitants on the planet, facilitate development in numbers and toward the year’s end 2018, it is relied upon to reach to 9.3 billion (Li, Leu, and Ji, 2014). In addition, China has risen as a tremendous market of the web. The quantity of web clients in China has surpassed than the clients of the web in the United States in 2008. In like manner, it is thought to be one of the quickest creating markets for portable clients also universally, with around 451 million clients of a PDA (To and Lai, 2014). Innovative advancements have enabled an extensive variety of contemporary capacities to PDA devices, encouraging numerous PDA budgetary administrations, similar to installment of bills, exchange of records, hand to hand exchanges, vicinity installments on the offering point, remote installments for obtaining the two administrations and products, and in addition distinctive kind of different offices like mobile phone showcasing, web based ticketing, rebates and coupons (Oliveira et al., 2016). In this unique situation, investigations of mobile payment as well as Development of Mobile Payment in China started directly after the simple first exchange of installment through cell phone made in 1997 (Dahlberg, Guo and Ondrus, 2015). The market for mobile payment in China is gigantic and the biggest over the world as far as size and potential for development. According to the investigation of iResearch (a web information specialist co-op of China) the portable installment market of China has come to ¥12.2 trillion of every 2016, which was ¥0.2 trillion out of 2012 while, the development is anticipated to be at ¥18.3 trillion (Coresight Research, 2018). In such manner, Ali pay entered in Chinese portable installment market and shook the general biological system in the Chinese market. At present, its control in the market of cell phone administrations from offices like taxi passages to individual to individual exchanges has not just made it a local name in a populace of 1.4 billion of China, be that as it may, a specialist organization of officeholder installment are being upheld to modernize or keeping the hazard lesser (Soo, 2017).

1.2 Objectives of the Study

The key focus of this research is to examine the development of mobile payment and its influences on the lives of Chinese locals.

- To evaluate the key success factor of mobile payment mode in China

- To analyze the cases of Ali Pay, WeChat and Apple Pay in the mobile payment market of China

- To assess the prime factors of success of Ali Pay, WeChat and Apple Pay in China’s mobile payment market

- To examine the Ali Pay’s competitive advantages upon its competitors such as WeChat and Apple Pay which makes the company a market leader in China mobile payment market

1.3 Rationale of the Study

1.3.1 Rationale of study and Problem Statement

The ideas of mobile payment (Development of Mobile Payment in China) are a relatively new zone to think about, less inspected when contrasted with other related regions of concentrate like online business, web or portable saving money (Oliveira et al., 2016). Sheltered and secure, solid and practical medium of installment is viewed as pivotal in the viable utilization of versatile business. Besides, portable installments are likewise called “m-installment” and “cell phone installments”. It is utilized to pay for profiting administrations or acquiring products, and also for the installment of bills or solicitations through a versatile device, as customary cell phone, android/advanced cell, or PDA, through having an advantage of portable system media communications or innovation of vicinities (Miao and Jayakar, 2016) However, it is also notable that all of these gaps in the research can be eradicated if the research will conduct critical and comprehensive research using both primary and secondary sources to assess the positive and negative impact of mobile payment development in different regions.

1.4 Significance of the Study

The significance of the study (Development of Mobile Payment in China) to draw the overall summary of the mobile payment including its technological terminologies where it will explain the advantages of the mobile payment and the using scope of the mobile payment in different medias or business channels where the buyer as well as seller are getting benefitted. Moreover, it is to show the significance of the success to China to become the biggest mobile payments market across the globe (Soo, 2017). Moreover, the growth of the internet and mobile users in China as mentioned earlier shows the significance of comprehension of this research.

CHAPTER TWO: RESEARCH METHODOLOGY

2.1 Introduction (Development of Mobile Payment in China)

In 2016, China’s mobile payment drastically duplicated in a motivating force to for the most part $5.5 trillion, as demonstrated by measurable looking over firm iResearch.1 That’s very nearly 50 times the estimation of the U.S. feature for versatile portion organizations, in light of Forrester Research’s measure of $112 billion for 2016 U.S. convenient payments.2 China’s startling 2016 improvement rate of 215 percent (from iResearch) was in like manner more than five times the U.S. improvement of 39 percent (from Forrester). This connection is tried by the manner in which that the bits of knowledge start from different sources which may portray “flexible portions” in a surprising way, anyway a study of various distinctive sources exhibits that the examination is directionally right. A couple of components are adding to China’s advancement in flexible portions, which frequently are portrayed as any trades made by wireless, paying little respect to whether for electronic business or at a physical location.3 They consolidate the quick improvement of online business, the spread of PDAs, the for the most part low choice of other portion procedures, for instance, charge cards, and the availability of convenient portion organizations from China’s gigantic Internet associations. Online business has expanded rapidly in China, regardless of the way that not as speedy as adaptable portions all in all: as demonstrated by iResearch, China’s electronic business rose 23 percent to about $3 trillion out of 2016. B2B bargains spoke to around 70 percent of the total, with little to-medium endeavors taking the greatest offer.

2.2 Research philosophy

Positivism, interpretivism and pragmatism are three research philosophies. According to Kumar and Phrommathed (2005), positivism is the research philosophy which beliefs in numeric data to reach an accurate result while interpretivism is a research philosophy which does not believe in numbers rather it believes in opinions and experiences of participants. On the other hand, Burns and Bursn (2000) stated that pragmatism talks about both numbers and opinions. This study is associated with positivism research philosophy because data from participants has been converted into numbers. This philosophy was suitable because users of Alipay can talk about its success through close-ended questions and their responses have been converted into numbers. Also, they were asked about the influence of payment apps on their lives. In addition, the comparison between the users of Ali Pay, WeChat and Apple Pay was easily carried out through the effective utilization of the positivism research philosophy. Therefore, this research philosophy is selected because there is a significant need for examining the perception of the mobile payment systems in the Chinese context along with examining Ali Pay, WeChat and Apple Pay. With this need for examining the perception of the consumers regarding different mobile payment systems, this philosophy has helped the researcher in establishing a causal relation between the study variables. This makes positivism philosophy more effective in the completion of study as compared to other philosophies.

2.3 Research approach

According to Kothari (2004), inductive research approach is used where theories are to be developed regarding a particular topic and such particular topic is made general through a detailed discussion of literature while deductive approach makes the topic very specific to reach a conclusion. A hypothesis is formed at the start of study which is tested at the end for acceptance or rejection. This research follows deductive approach because the topic does not require the development of any theory but the success of Alipay and influence of mobile payment apps can be determined through deductive approach, therefore, such approach was suitable as a hypothesis has been formed. In addition to this, the researcher has opted for deductive approach considering the nature of the study because the researcher is intended towards examining the comparison between Ali Pay, WeChat and Apple Pay from the perspective of the customers regarding mobile payment system. Therefore, the adoption of a deductive approach helped the researcher in developing theoretical basis through quantitative data and the testing hypothesis of the study.

2.4 Research design

This research follows quantitative design because responses of users of Alipay have been converted into numbers and the use of qualitative would have taken more time and sample size would have been lower for interviews. Further, there was no need for interviews because close-ended questions sufficiently achieved the objectives of the study. In addition to the above statement, the researcher intended to assess the prime factors of success of Ali Pay, WeChat and Apple Pay in China’s mobile payment market, therefore, the selection of quantitative research design is most suitable design because it has helped the researcher in figuring out the perception of the customers of Ali pay, WeChat and Apple Pay in China.

Fragment 1: Which is better

- Looked after Equipment

- Apple Pay just sponsorships Apple contraption with unique finger impression.

- WeChat bolsters the a lot of PDA with WeChat application.

- Alipay is general for all moved cell, tablets, and PC.

- Apple Pay made in ios framework, no require with any applications. While the other two are distant bit applications, need to selection.

- Bit Process

- Basic segment with Apple Pay

- With Apple Pay can make checkout withdrew, basically put the iPhone or Watch close contactless per user, with the finger hold the Home catch to fingerprinting. No persuading inspiration to open any App or open the telephone or screen.

- Complex bit courses of action with WeChat Wallet and Alipay

- They have to run the contraption, enter applications under a conspicuous structure, by then star to pay by isolating the QR code by then enter the secret key or exceptional stamp checking, at last do divide accreditation.

Fragment 2: Features and Security

Apple Pay can pull back trade out ATM

Apple Pay have avoided with monetary exchanges, when checkout, cash is especially from the cards which accumulated with. In addition, Apple Pay account data will be encoded, and without your novel stamp certification others can’t move your card property.

Apple Pay can be utilized to pull back trade unmistakably out the bank ATM machine with a NFC contraption.

WeChat wallet and Alipay can manage back and offer amazing City Service

For these two are the pariah applications, they can oversee exchange out its record, and there’s different cutoff points can be use to serve life. For example, open a record, store cash, money related association, particularly in web back.

Both Wechat wallet and Alipay are progressing different City associations. Clients can book long segment transportation, pay improvement fines, expenses and yearly auto selection through the association, over enlisting for marriage or work. Extra, Red envelopes pressed with money talented to loved ones is a particularly comprehended with Chinese.

Pros and Cons:

Apple Pay: Security is generally high, pay step clear and fine, don’t need to pay for systems association, getting a charge out of shorter bit time, can pull back trade out ATM machines like bank cards.

Notwithstanding, just sponsorships Apple gadgets, the measure of bank card underpins not as much as would be typical, high checks to fragment, the line arrangement isn’t completely made, have not could square away right away development address a peril to WeChat and Alipay in China.

WeChat and Alipay: high recognition, low impediments to territory, you can in like way purchase budgetary things, get a red envelope.

Regardless, parcel preparing astonishing and defenseless against maladies and Trojans (in a general sense Android telephone) intrusion drive forward through budgetary affliction.

2.5 Data collection method

There is used the collection of primary data and the source of secondary data. Here, primary data source are te internal sources that is gathered from primary knowledge aboiut the development of mobile payent and influence of it which is directly extracted by researcher solely for current study and secondary data is the data is collected from internet sources. In this context, the researcher has collected both primary and secondary data for authenticating the results of this research and contributing significantly towards the database. The primary data has been collected from the users of Ali Pay, WeChat and Apple Pay which are operating in China’s mobile payment market. The users have provided their valuable insights regarding the mobile payment system present in China. On the other hand, the secondary data has been collected from the secondary sources such as journal articles, reports and articles for presenting the literature review of the study which is related to the concept of mobile payment in China and other related factors.

2.6 Research instrument

According to Neuman (2013), a research instrument is the tool used to collect data for the research; it can be a questionnaire, interview, survey, poll, annual report etc. This study has used the questionnaire as research instrument because the questionnaire can be distributed to a sufficient number of users while researcher would not have been able to conduct interviews from that much number of users. Additionally, there was no need for interviews or other qualitative data because the topic does not require detailed responses. The questionnaire has been designed on 5 points Likert scale based on close-ended questions.

2.7 Sampling

Wiersma and Jurs (2005) stated that for this research, 100 participants are selected to distribute questionnaires, this is a sufficient number because it is practicable and they represent the population well. Most of the researches use 100 as a sample size because the number is neither very large to make it difficult for the researcher nor too small to not represent the population fairly. In this research, the researcher has focused on the sample of 100 customers of Ali Pay, WeChat and Apple Pay who have reflected on China’s mobile payment market. These are particularly considered for the use in the study due to ease of reach and accessibility. Therefore, the population has been used which was effective for the results of the study.

2.8 Sampling technique

According to Nielsen and Einarsen (2008, p.268), probability sampling refers to sampling in which each participant within the population is given a fair chance of selection while non-probability sampling does not give fair chance to each participant. This research is based on non-probability sampling category in which convenience sampling method is selected. This methods are picked since they are least complex to select for the examination and the examiner did not consider picking subjects that are illustrative of the entire people.In a wide range of research, it is immaculate to test the entire people, yet when in doubt, the masses is just excessively tremendous that it is troublesome, making it impossible to join every individual. This is the inspiration driving why most investigators rely upon assessing frameworks like convenience analyzing, the most broadly perceived of all testing methodology. Various authorities slant toward this inspecting technique since it is fast, sensible, basic and the subjects are expeditiously open. This method was suitable for the research because finding Alipay users was a bit difficult task so to save effort and time of the researcher, convenience sampling was used.

2.9 Data analysis plan

According to Mackenzie and Knipe (2006, p.196), data analysis plan is made according to the type of data to be analysed. For the data analysis in this research, the researcher has used SPSS software in order to analyse the responses generated from a questionnaire filled out by the users of Ali Pay, WeChat and Apple Pay. This has helped the researcher in assessing the success factors of these companies with respect to the mobile payment system in China. The data in this research was inserted into SPSS software for giving it a meaningful form and transforming it for the data analysis. The test which has been used in this research includes demographic analysis, frequency analysis along with correlation and regression analysis.

2.10 Ethical guidelines

The researcher has followed a few ethical guidelines, therefore, this research is considered reliable. The researcher has avoided plagiarism during documentation of information and has added a reference to the person whose work has been used. Further, participants were told the reason and purpose of the survey and only those participants were included in the research that was willing to respond. The contact information of participants has been kept confidential and no participant was harmed while conducting this research. Furthermore, the researcher has documented the information honestly without including any personal statements in the research.

2.11 Limitations of research

This research is affected by a few limitations without any fault of the researcher and due to such limitations research scope is limited. Therefore there is found to many data coolection limit.

CHAPTER THREE: LITERATURE REVIEW (Development of Mobile Payment in China)

3.1 Introduction (Development of Mobile Payment in China)

The current section of the research study is determined to review the literature that will focus on the development of mobile payment in China. The main purpose of analyzing the notion and paradigm of mobile payment in China is based on evaluating the fact that how mobileo payment emerged and gained significance in China. In addition to this, the current section of the research study also identifies the factors that have influenced the development of mobile payment applications in the Chinese mobile payment industry. Most importantly, this section of the research study entails past studies, peer-reviewed articles, case studies of Alipay, WeChat, and Apple Pay and in order to appropriately develop the research based on the theoretical and conceptual framework.

3.2 Concept of Mobile Payment in China

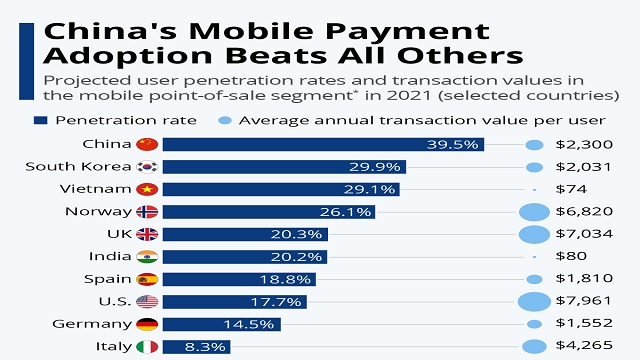

A study conducted by Dahlberg, Guo, and Ondrus (2015)indicates that the concept of mobile payment or m-payment is considered as utilization of a portable electronic device such as mobile phone, laptop, or tablet to buy products online. The concept of mobile payment is also based on the fact that it uses the Internet of Things (IoT) in order to purchase products online. Moreover, it has also been assessed that with the development of integration between the internet of technology and mobile-based communication, China has managed to attract a large number of mobile payment of users. In recent times, it has been reported that more than 60% of the total urban population in China are currently using mobile payment as an alternative to traditional shopping or product purchasing system (To and Lai, 2014). The mobile payment penetration rate in China is highlighted in the figure below,

A survey was conducted by Qu, et al. (2015) in order to assess the emergence of mobile payment in China. The result obtained from the research study indicates that the mobile-payment adoption in China is critically influenced by different reasons or factors such as service quality, system quality, social influence, usefulness, and trust. In this way, it could be articulated that the influence of service quality and system quality of decisions of individuals in China is significant in the region.

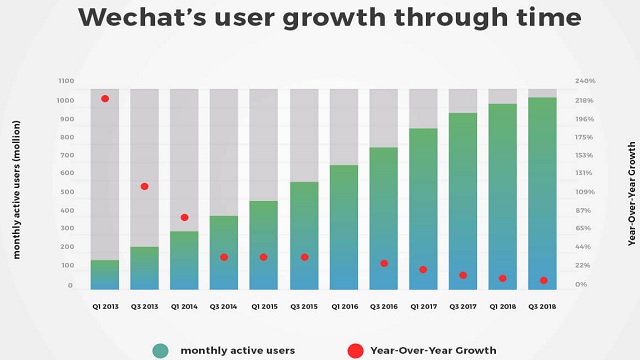

On the other hand, another study conducted by Yang, et al. (2015) illustrates that with the explore growth and development in the field of information and communication technology, many local and multinational firms functioning in China have managed to introduce online retailing website. These online retailing websites emerged as a new approach to the electronic commerce, which only entailed the electronic or digital payment technique. In addition to this, the mobile payment approach is relatively more convenient for users in China. As a result, numerous banks and other financial institutions in China have introduced mobile payment facilitation system through a mobile application. In this way, instead of carrying cash, or debit card or credit card, payment could be made through mobile payment expediently without being exposed to the risk of theft. Meanwhile, mobile payment information is encrypted during the transmission which makes it a safer payment method than a debit card or credit card (To and Lai, 2014). Since, mobile payment is an exchange of money from one buyer to seller without physical contact and to oblige payments this type of process make it safer, private, and convenient than any other system. It is a noticeable fact China has an extensive population of the internet and mobile users. The respective statement can be further approved by reviewing the study of Qu, et al. (2015) in which it has been reported that the total number of smartphone users reached 1200 million in the past five years. Furthermore, it has also been reported that nearly 300 million are using the 3G network. The extensive number of smartphone and 3G users in China indicates the extensive use of mobile payment in China. There has been increasing number of users for the mobile payment which is depicted in the graph below,

Fig: mobile payment platforms worldwide

A study conducted by Tea, et al. (2015) reports that that in the last two to three years, the development of mobile payment, exclusively remote payment has experienced extensive growth in China due to maturity of the 3G network, the instigation of the unified payment standards, and availability of diversified applications. The significant of mobile payment in China can be further understood by reviewing the fact that the total scale of mobile payment in the country (China) apparently exceeded $28.5 billion with an annual growth of 89.2%. It has been projected that the mobile payment will expectedly experience more growth and development in the region as it has been reported by “Ministry of Industry and Information Technology” in China that the market of the third party mobile payment service is growing exponentially and attracting billions of smartphone users in China (Miao and Jayakar, 2016).

On the other hand, it is also a notable fact that the growth in the field of mobile payment has significantly impacted the lives of citizens in China. For example, people nowadays in China are seen using mobile payment (third party applications) to go shopping, buy tickets, pay utility bills, and take the public transportations as well (Qu, et al., 2015). In the olden days, Chinese citizens used to rely on cash to buy products and services. However, it has been revealed by To and Lai (2014) that that cash-based payment system has notably been replaced by the emergence of mobile payment.

A study conducted by Oyewole et al. (2013) also highlights that the concept of mobile payment has turned out to be a type of lifestyle in China. As a result, most of the people living in China are doing more consumption, payments, and trading on the third party mobile services such as Alipay and WeChat payment. In this way, it becomes evident that Chinese society has somehow become more advanced with the emergence of the mobile payment approach in China. As a result, the mobile payment approach has massively influenced the lives of Chinese people by providing them with a platform to do transactions, purchasing, and trading via smartphone.

Figure: Rise of WeChat Pay in China

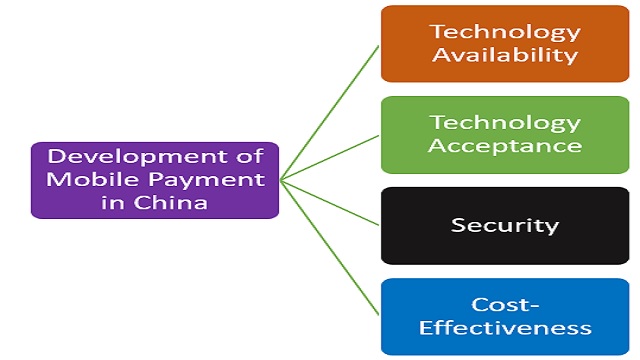

3.3 Key Factors Influencing Development Mobile Payment in China

It has already been discussed above that the development in the field of the mobile payment has managed to attain immense value and significance in China. In this concern, this section of the research study will elaborate the main reasons or factors which are influencing the development of mobile payment in China.

3.4.1 Adaptability of technology by the people

A study conducted by Zhong and Nieminen (2015) illustrates that one of the major factors which influence the development of mobile payments in China is based on the fact that people in China are highly enthused by the concept of using smartphone and Internet of Things (IoT) in order to bring simplification in their lives. In this manner, it has been observed that many people are passionate regarding the use of technological features like e-commerce and m-commerce (mobile payment) to pay bills and buy products and services online. It has been further assessed by Zhong and Nieminen (2015) that if the end user is not familiar with mobiles or such payments through mobiles, the transition to mobile payments will become difficult. Hence, if the users are not going to adapt to technology, the development of the technological feature will be difficult. Adversaries to new technology are created by minds not willing to change or not to accept the transformation. It also depends on the demographics of the people who are the onset of facing new technology. Furthermore, the age of the citizens of China also impacts the usability of mobile payment technology. Older age group find difficulties in adapting to changing environments whereas younger aged citizens might be swift in adapting to the new technological change. (Zhong and Nieminen, 2015) The above analysis raises a key question or concern that whether the rejection of older people to use third-party applications for mobile payment will prove to be detrimental for mobile payment approach in China or not.

3.4.2 Availability of High-Quality Technology in China

It has been discussed earlier that China is very advanced in the use of mobile phones and the Internet of Things (IoT). A study conducted by Baek (2015) also approves the above statement by articulating that the government of China has recently invested more than $10 billion in the field of Information and Communication Technology (ICT). Therefore, the technology is greatly valued and easily accessible by users in the country (China). The significant of technology in the development of mobile payment can also be further understood by reviewing the study of Qu, et al. (2015) in which it has been clearly stated that if the infrastructure of mobile technology did not exist in the country, there would be no possibility of initiating mobile payments as the mobile payment method is significantly dependent on the existence of mobile technology.

Moreover, the availability of technology here refers to the availability of mobile phone signals in the region where payment needs to be made. If there is no mobile coverage (Lee, 2015), the users will not prefer to make payment through mobiles, and hence will not rely on the system. In this way, it could be stated that the availability of high-quality technology in China has contributed to the development of mobile payment in China.

3.4.3 Cost of making mobile payment

In order to make the payments system viable and highly adopted by the people of the country, it should be cost-efficient. This is an important factor, as the use of mobile phone in making payments should be very cost-effective to be adopted by the people (Hamzeh, 2013). The cost of making a payment from the point of the end-user includes the cost of purchasing a mobile phone, and a mobile connection and the payment application to be installed on the phone. These costs should be within reach of common man to make it viable for him to make such transactions.

On the other side, the back end of operating a mobile payment application will also incur costs. Companies such as Wechat pay and Alipay will need to install an infrastructure to facilitate payment through a mobile phone. This includes the development of a system to maintain money accounts of the people and negotiating payments with merchants and customers. In such condition, a major question arises that whether the installation of new infrastructure will restrict the development of mobile payment in China or not.

3.4.4 Security in Mobile Payment in China

The above analysis highlighted the contribution of extensive resources and technologies in the development of mobile payment. However, I personally believe that the implication of the security is also a major factor which has convinced users in China to make use of the mobile payment procedure. In case, if the customers were not willing to use the mobile payment in China, then the entire investment, implication of technology, and resource would have failed to make a significant impact or influence on the development of the mobile payment procedure. A study conducted by Li, Liu, and Ji (2014) also state that the behaviour of the customer has a specific role in the growth and development of a technological feature.

The study further indicates that in terms of online payment, users are highly enthused by the concept of security. Since mobile payment due to effective encryption technique is highly secured. Therefore, the integration of security in the mobile payment is serving as a key factor which enhances the development of mobile payment in China. However, it has also been observed that several cases of online theft and security breach have emerged in the online payment procedure, in this way, a major question arises that whether these cases/ incidents of online theft will negatively affect the development of mobile payment in China or not.

3.5 Overview of Chinese Mobile Payment Market

According to a news article published by South China Morning Post (2018), there are two well-known companies which are functioning as the third online party service in the mobile payment market of China. These two companies are Alipay and WeChat pay. It has been noted that Alipay is the affiliate of Alibaba which is a giant online retailer in China and also throughout the world. The South China Morning Post further goes on to say that, Alipay and WeChat pay is popular among the high net worth individuals of China. The market in China is dominated by Alipay followed by WeChat pay. Ranking of methods of payment is such that mobile payments are at the top, followed by mobile cards and lastly physical cash (South China Morning Post, 2018). The methods used by AliPay and WeChat include POS tapping, swiping or checking in with a mobile phone. The checking in also supports NFC (near-field communication and QR codes readable by machines).

Mobile payments have gone ingrain in the economy of China as a very popular medium of payment settlement. Mobile payments are popularly used in supermarkets, shopping malls, dining outlets and even with small-scale vendors. The system is further being enhanced by the use of mobile payment watches and wristbands and expands to transactions to be made abroad. The total volume of transactions made through mobile phone platform in the mainland China was approximately 30 trillion Yuans only in the third quarter of 2017.

This figure is almost tripled that of the same figure of 2016, whereas, the figures of ten months of 2016 totaled 81 trillion Yuan (South China Morning Post, 2018). This means that the market has majorly adopted the methods of payments through mobiles and is going cash free in the future. The country of China has exceeded the United States in the volume of mobile phone payments. The number of transactions has also increased. Apart from this, it has also been appraised that there is another newly introduced third party application for mobile payment in the market of China known as Apple Pay is termed as a mobile payment/ digital wallet service initiated by Apple Inc. This online payment service enables users to make an online payment with the help of iOS apps which can be executed on iPhone, iPad, Mac, and Apple Watch (Liu and Zhou, 2017).

3.6 Comparison of Main Third Party Applications for Mobile Payment in China

In this section of the research study, a comparison will be made among the key players in the mobile payment market of China. The advantages and disadvantages of all three identified third-party applications for mobile payment will be made. Additionally, it will be analyzed that which third application party is considerably more prominent in the mobile payment market of China.

In terms of supportive equipment, the main advantage of WeChat Pay is that it can be used in all smartphones which have WeChat App (iSUmsoft, 2018). In contrast, Apple Pay is termed as disadvantageous as it can only be used in smartphone gadgets which are launched by Apple, Inc. In addition to this, it has been appraised AliPay easily attains a competitive advantage over these two third-party applications as Alipay can be easily accessed on all smartphones, tablets, laptops, and personal computers. However, in terms of payment method, Apple Pay offers a much effortless and straightforward method for payment whereas in AliPay and WeChat Pay, the users have to follow a specific procedure for making a mobile payment (iSUmsoft, 2018).

Apple Pay is also much secured, but it has several barriers to entry (iSUmsoft, 2018). In such condition, Ali Pay with its great convenience, popularity, and low barrier to entry has turned out to the number one-third party mobile payment service in China. In this regard, the role of Alipay in the mobile payment market of China will be elaborated.

3.7 Role of Alipay in Mobile Payment Market of China

It has been noted that Alipay is owned by Ant Financial Services, it serves approximately 300 million customers in China and also few million abroad (Liu, 2015). About 54% per cent of the transactions were made from mobile phones located in rural areas. Hence, it becomes evident that with the emergence of Alipay, the market of China has become changed as now not only people in the urban areas of China are using mobile payment. In fact, people residing in rural areas have also started to use mobile payment due to the easy interface and procedure provided by Alipay in China.

A study conducted by Liu (2015) also states that Alipay is a major player of Chinese mobile payment market. In terms of market share, it leads WeChat by a significant percentage. Since being the leader in the mobile phone market, it has a role to play. It should ensure the safety of its customer’s wealth that is held by the company. It should play a positive role in enhancing the security of the payment system (Kumar, 2013) and make it more reliable in the eyes of new users of the online third-party payment market.

Secondly, Alipay is enjoying a large market share hence it is also utilizing the economies of scale applicable to the mobile payment system. The scale of operations reached by Alipay is difficult for others to reach; hence there will be tough competition for others trying to reach the position. The role to be played by Alipay is that of a monopoly, which means it can exploit consumers. Hence the company should take measures to reduce prices. Further, it also has the duty to promote harmony among the competitors. It supports the e-commerce industry in China by operating a multi-function payment platform (Liu, 2015).

Alipay plays a crucial role in the e-commerce business in China; it features online payment, online retail and wholesale, telecommunications, utilities, financial services and virtual gaming. Alipay is popular in China and has its own resources. Its products features are unique and suit the preferences of Chinese consumers.

3.8 Theoretical Framework

The theory presented by Dahlberg (2015), states that payment instruments, habits, and methods have a competition with one another to attract the attention of people interested in making an exchange of wealth. This theory requires that either the payment from the mobile phone should increase the productivity of executing the transaction or decrease the cost of it.

On the other hand, the additional theories which comply or validates the above analysis regarding the concept of mobile payment and its impact on the lives of individuals will be elaborated below.

3.8.1 Technology Acceptance Model

The technology acceptance model is termed as a theory of information system which indicates how a user accepts and uses new technology (Marangunić and Granić, 2015). It has been assessed that users tend to accept a theory based on two main features of the application. At first, if the application is easy to use and if the application is advantageous. Since mobile payment is both easy to easy and advantageous as well. For this reason, the mobile payment technology has gained significance in China.

3.8.2 Value-Based Adaption Model

A value-based adaption model indicates that people adopt new technological features and model is the respective model/feature is termed as valuable by them (Lin and Lu, 2015), In this way, it becomes evident that value-based model assists in explaining the adoption of mobile payment in China from the perspective of value maximization. Hence, it could be stated that most of the people adopt mobile payment method in China due to the reason that it provides maximum value and benefit to individuals in the society.

3.9 Conceptual Framework (Development of Mobile Payment in China)

3.10 Summary of Literature (Development of Mobile Payment in China)

It has been identified in the literature that the development of mobile payment system (Development of Mobile Payment in China) is vital in the economy of today as most of the buyers opt to make payment through Alipay application in the mobile phone. The process of making payment via mobile payment is much easier as compared to other means of payments such as cheque or cards. For this reason, it has been considered that people in China have accepted the mobile payment due to the easiness, convenience, and security in the mobile payment procedure. In addition to this, it has also been assessed that the development of mobile payment has significantly impacted the lives of individuals in China as it has allowed them to do online shopping, pay utility bills, and purchase tickets in a secure environment.

3.11 Gaps in Research

Based on the above findings (Development of Mobile Payment in China), it becomes evident that there are different viewpoints and perception regarding the development and use of mobile payments. In this regard, the main gap in the research which somehow limits or confines the applicability of the current research study is that it has only focused on the single perception or viewpoint regarding the use of mobile payment. For example, the research study has only focused on the benefits which are attained by consumers in China from using third-party applications for mobile payment whereas the consequences which are faced by individuals in using third-party applications for mobile payment has been ignored. In a similar way, the unavailability of the primary sources also somehow limits the applicatively of the research study. Moreover, the research study only focused on China’s mobile payment market whereas the mobile payment has gained immense popularity in different parts of the world. However, it is also notable that all of these gaps in the research can be eradicated if the research will conduct critical and comprehensive research using both primary and secondary sources to assess the positive and negative impact of mobile payment development in different regions.

Findings (Development of Mobile Payment in China)

For most Chinese experts, the wide example toward the usage of phones to make portions is a condition of pride in the nation’s mechanical progress.

While the national bank’s stresses are upheld, rushed mediation could abbreviate the astonishing pace of private-part headway of new organizations and developments in the country.

The rising in versatile portions has incited an awesome deceleration in the advancement in the proportion of exchange out stream in China. Beyond question, the advancement rate of cash stream has been running underneath that of the economy since 2014. For example, the volume of exchange out course grew 6.4% a year back while the economy expanded 6.7%.

Little portions settled in genuine cash have for a long while been out of the degree of the bank clearing structure. Somewhat, national financial specialists could neglect this on account of specific difficulties in following such trades.

Nevertheless, the cashless example could change national banks’ incredibleness in the clearing system. Under the present arrangement of activity of convenient portions, Ant Financial and Tencent go about as specialists among customers and banks to complete money trades beginning with one record then onto the following.

As a result, these web associations by and by have full control of all information as for customers’ flexible portion trades. To a particular degree, web associations seem to have set up a self-governing clearing structure for little trades in parallel to the interbank clearing system controlled by the national bank.

The cashless example could in like manner make it more troublesome for the national bank to screen capital streams transversely over edges. Since the astonishing debasing of the yuan in August 2015, China’s national bank has battle distinctive sorts of disguised capital outpourings to avoid an interminable circle of capital flight and cash debasement.

Finally, the cost of tight order over versatile portions could be high. Both Ant Financial and Tencent have contributed seriously to collect relations with banks to build up their own specific portion stages. The establishment of China Nets Union has completely crushed the estimation of their present stages and killed this favored point of view over new players in the flexible portion publicize.

Conclusion (Development of Mobile Payment in China)

In this examination (Development of Mobile Payment in China), we have researched purposes behind individuals to grasp Mobile payment in China by considering a game plan of factors influencing Mobile payment recognized from the written work. This examination watched out for the data gaps in the domain of Mobile payment gathering generally speaking and in China especially. The results of this examination demonstrates customers’ desire to use Mobile payment in China is affected by various components, tallying customers’ properties, system and organization quality, handiness, social effect and trust. Among them, structure quality to the extent convenience additionally, advantage quality regarding openness have strong impacts. Moreover, headway by the authority associations and customers’ need and particular individual lifestyles have been found as new fundamental factors impacting the Mobile payment adaption. By exploring the effect of these parts on Mobile payment gathering, we can all the more promptly appreciate why individuals use or not to use Mobile payment.

This examination offers humble promise to industry and research related to Mobile payment choice. Concerning industry, the eventual outcomes of the examination can possibly help expert associations to all the more promptly fathom clients’ wants and factors that impact their decision to use Mobile payment. Along these lines, better organizations can be given and better systems to propelling Mobile payment can be planned. For example, Mobile payment providers can propel the organization by offering discounts or distinctive inspirations. They can in like manner improve the system quality and organization quality by ensuring the achievement of trades, keeping the movement straightforward and broadening the degree of availability. From an academic perspective, this examination adds to the present Mobile payment composing which is correct currently led by quantitative examinations and offers accommodating starting encounters into purposes behind individuals to grasp Mobile payment especially in China. It may in like manner raise the premiums of various pros in practically identical zones to approach the examination using an emotional procedure to supplement existing quantitative examinations that at present overpower the written work. In light of the degree and the time distribution of this examination, there are couple of confinements of this examination. Immediately, the proportion of research test is pretty much nothing and in this manner the disclosures can’t be summed up to the entire Mobile payment customers. In addition, simply individuals who have contribution in using Mobile payment were picked as the case. The all inclusive community without the experience of using Mobile payment were not considered. It is significant to fuse non-customers later on concentrates to also examine purposes behind not using Mobile payment. Finally, the examination just explored Mobile payment determination in China. Assorted countries may be at different periods of Mobile payment progression and thusly clarifications behind using Mobile payment may differentiate from what have been recognized in this examination. Future research coordinated in different countries would along these lines be gainful to furthermore refine the stream understanding around there of Mobile payment choice.

References (Development of Mobile Payment in China)

Baek, Y. M. (2015). Current status of E-commerce market in China and implication. Journal of Digital Convergence, 13(1), 111-124.

Burns, R.B. and Burns, R.B., 2000. Introduction to research methods.

Coresight Research. 2018. Deep Dive: Mobile Payments in China. <https://www.fungglobalretailtech.com/research/deep-dive-mobile-payments-china/>

Dahlberg, T., 2015, August. Mobile Payments in the Light of Money Theories: Means to Accelerate Mobile Payment Service Acceptance?. In Proceedings of the 17th International Conference on Electronic Commerce 2015 (p. 20). ACM.

Dahlberg, T., Guo, J. and Ondrus, J., 2015. A critical review of mobile payment research. Electronic Commerce Research and Applications, 14(5), pp.265-284.

Dahlberg, T., Guo, J., & Ondrus, J. (2015). A critical review of mobile payment research. Electronic Commerce Research and Applications, 14(5), 265-284.

Dahlberg, T., Mallat, N. and Öörni, A., 2003. Trust enhanced technology acceptance modelconsumer acceptance of mobile payment solutions: Tentative evidence. Stockholm Mobility Roundtable, 22, p.23.

Ghezzi, A., Renga, F., Balocco, R. and Pescetto, P., 2010. Mobile Payment Applications: offer state of the art in the Italian market. Info, 12(5), pp.3-22.

Gupta, S., 2013. The mobile banking and payment revolution. European Financial Review, 2, pp.3-6.

Hamzeh, M., Globaltel Media Inc, 2013. Mobile-to-mobile payment system and method. U.S. Patent 8,369,828.

Heredia Salazar, R., 2017. Apple Pay & Digital Wallets in Mexico and the United States: Illusion or Financial Revolution?. Mexican law review, 9(2), pp.29-70.

iSUmsoft. (2018). Compare Apple Pay with Alipay and WeChat Pay. Retrieved August 31st, 2018, from https://www.isumsoft.com/apple/compare-apple-pay-with-alipay-and-wechat-pay.html

Kang, S., 2014. Factors influencing intention of mobile application use. International Journal of Mobile Communications, 12(4), pp.360-379.

Kessel, K.A., Vogel, M.M., Alles, A., Dobiasch, S., Fischer, H. and Combs, S.E., 2018. Mobile App Delivery of the EORTC QLQ-C30 Questionnaire to Assess Health-Related Quality of Life in Oncological Patients: Usability Study. JMIR mHealth and uHealth, 6(2).

Kothari, C.R., 2004. Research methodology – Development of Mobile Payment in China: Methods and techniques. New Age International.

Kumar, R. and Rajalakshmi, S., 2013, December. Mobile cloud computing: Standard approach to protecting and securing of mobile cloud ecosystems. In Computer Sciences and Applications (CSA), 2013 International Conference on (pp. 663-669). IEEE.

Kumar, S. and Phrommathed, P., 2005. Research methodology (pp. 43-50). Springer US.

Kumar, S., Nilsen, W.J., Abernethy, A., Atienza, A., Patrick, K., Pavel, M., Riley, W.T., Shar, A., Spring, B., Spruijt-Metz, D. and Hedeker, D., 2013. Mobile health technology evaluation: the mHealth evidence workshop. American journal of preventive medicine, 45(2), pp.228-236.

Lee, J.C., British Telecommunications PLC, 2015. Cellular communication system comprising macro and micro cells. U.S. Patent 8,934,911.

Li, J., Liu, J. L., & Ji, H. Y. (2014). Empirical study of influence factors of adaption intention of mobile payment based on TAM model in China. International Journal of u-and e-Service, Science and Technology, 7(1), 119-132.

Li, J., Liu, J.L. and Ji, H.Y., 2014. An empirical study of influence factors of adaption intention of mobile payment based on the TAM model in China. International Journal of u-and e-Service, Science, and Technology, 7(1), pp.119-132.

Lin, K. Y., & Lu, H. P. (2015). Predicting mobile social network acceptance based on mobile value and social influence. Internet Research, 25(1), 107-130.

Liu, L., & Zhou, M. (2017). Empirical study of influencing factors of the users’ intention based on the survey of apple pay users. Journal of Interdisciplinary Mathematics, 20(6-7), 1391-1395.

Liu, R. (2015). The role of Alipay in China. Netherlands: Faculty of Science, Radboud University.

Liu, R., 2015. The role of Alipay in China. Netherlands: Faculty of Science, Radboud University.

Lu, Y., Yang, S., Chau, P.Y. and Cao, Y., 2011. Dynamics between the trust transfer process and intention to use mobile payment services: A cross-environment perspective. Information & Management, 48(8), pp.393-403.

Mackenzie, N. and Knipe, S., 2006. Research dilemmas: Paradigms, methods and methodology. Issues in educational research, 16(2), pp.193-205.

Mackey, A. and Gass, S.M., 2015. Second language research: Methodology and design. Routledge.

Marangunić, N., & Granić, A. (2015). Technology acceptance model: a literature review from 1986 to 2013. Universal Access in the Information Society, 14(1), 81-95.

Marczyk, G., DeMatteo, D. and Festinger, D., 2005. Essentials of research design and methodology. John Wiley & Sons Inc.

Miao, M. and Jayakar, K., 2016. Mobile payments in Japan, South Korea, and China: Cross-border convergence or divergence of business models?. Telecommunications Policy, 40(2-3), pp.182-196.

Miao, M., & Jayakar, K. (2016). Mobile payments in Japan, South Korea and China: Cross-border convergence or divergence of business models?. Telecommunications Policy, 40(2-3), 182-196.

Neuman, W.L., 2013. Social research methods: Qualitative and quantitative approaches. Pearson education.

Nielsen, M.B. and Einarsen, S., 2008. Sampling in research on interpersonal aggression. Aggressive Behavior: Official Journal of the International Society for Research on Aggression, 34(3), pp.265-272.

Okazaki, S., 2006. What do we know about mobile Internet adopters? A cluster analysis. Information & Management, 43(2), pp.127-141.

Oliveira, T., Thomas, M., Baptista, G. and Campos, F., 2016. Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Computers in Human Behavior, 61, pp.404-414.

Osang, F.B., Ngole, J. and Tsuma, C., 2013, February. Prospects and Challenges of Mobile Learning Implementation in Nigeria. Case Study National Open University of Nigeria NOUN. In International Conference on ICT for Africa (pp. 20-23).

Oyewole, O.S., El-Maude, J.G., Abba, M. and Onuh, M.E., 2013. Electronic payment system and economic growth: a review of transition to cashless economy in Nigeria. International Journal of Science, Engineering, Technology, 2, pp.913-918.

Perez, G., Dalla Rosa, A., Medeiros Jr, A. and Comar, M., 2013. Trends in the Use of Mobile Payment in Brazil: An Analysis Using the Delphi Method. In CONF-IRM (p. 49).

Qu, Y., Rong, W., Ouyang, Y., Chen, H., & Xiong, Z. (2015, December). Social aware mobile payment service popularity analysis: the case of wechat payment in China. In Asia-Pacific Services Computing Conference (pp. 289-299). Springer, Cham.

Soo, Z. 2017. China’s mobile payment giants forcing incumbents to innovate. South China morning post. China Tech. <https://www.scmp.com/tech/china-tech/article/2124512/chinas-mobile-payment-giants-forcing-incumbents-innovate>

South China Morning Post. (2018). China moves towards cashless society as Alipay, WeChat Pay gain. [online] Available at: https://www.scmp.com/business/companies/article/2130400/china-moves-further-towards-cashless-society-payment-giants [Accessed 16 Aug. 2018].

Teo, A. C., Tan, G. W. H., Ooi, K. B., & Lin, B. (2015). Why consumers adopt mobile payment? A partial least squares structural equation modelling (PLS-SEM) approach. International Journal of Mobile Communications, 13(5), 478-497.

To, W. M., & Lai, L. S. (2014). Mobile banking and payment in China. IT Professional, 16(3), 22-27.

To, W.M. and Lai, L.S., 2014. Mobile banking and payment in China. IT Professional, 16(3), pp.22-27.

Wiersma, W. and Jurs, S.G., 2005. Research methods in education: An introduction.

Yang, S., Lu, Y., Gupta, S., Cao, Y. and Zhang, R., 2012. Mobile payment services adoption across time: An empirical study of the effects of behavioral beliefs, social influences, and personal traits. Computers in Human Behavior, 28(1), pp.129-142.

Yang, Y., Liu, Y., Li, H., & Yu, B. (2015). Understanding perceived risks in mobile payment acceptance. Industrial Management & Data Systems, 115(2), 253-269.

Yusuf, M.B.O., Ghani, G.M. and Meera, A.K.M., 2017. The challenges of implementing gold dinar in Kelantan: An empirical analysis. Institutions and Economies, pp.97-114.

Zhao, Y. and Kurnia, S., 2014. Exploring Mobile Payment Adoption in China. In PACIS (p. 232).

Zhao, Y., 2017. Research on the consumer finance system of Ant Financial Service Group. American Journal of Industrial and Business Management, 7(05), p.559.

Zhong, J., & Nieminen, M. (2015). Resource-based co-innovation through platform ecosystem: experiences of mobile payment innovation in China. Journal of Strategy and Management, 8(3), 283-298.

Written by

Email: [email protected]